Insights

Payment Orchestration Platform: Solutions for Businesses

POP: Definition, Components, and Solutions for Businesses

Payment Orchestration Platform – this term refers to a unified set of tools and services that streamline how businesses handle digital payments across multiple providers. In simple terms, a payment orchestration platform is a centralized hub that connects to various payment service providers (PSPs), gateways, and payment methods, coordinating every step of a transaction from start to finish. By doing so, it allows an enterprise to manage all payment processes in one place, rather than dealing with each provider separately.

How It Works POP and Why It Matters

A payment orchestration platform acts as the “conductor” of your payment ecosystem, ensuring each part (gateway, acquirer, fraud check, etc.) works in harmony. When a customer checks out on your site, the orchestration layer dynamically routes the payment to the optimal provider based on predefined rules (e.g. transaction amount, customer location, or cost). It handles authentication (like 3-D Secure for card payments), authorization (securing an approval from the bank), and even settlement of funds, all while applying smart logic such as retries or cascades if a payment fails. Essentially, the platform automates what would otherwise be manual or separate processes, resulting in higher success rates and a smoother payment flow.

Why is this important for enterprises? First, it boosts revenue by enhancing approval rates – the platform can retry declined transactions via backup gateways and find a path to approval where a single provider might fail. Merchants have reported increasing their approval rates by up to 20% using smart routing and automated retries, and conversion rates by up to 30% with cascading failovers. Second, it reduces costs by routing transactions in the most cost-effective way (for example, using a local acquirer to avoid cross-border fees). Third, it improves customer experience – customers can pay with their preferred method and get faster, more reliable checkouts, leading to fewer cart abandonments. Finally, it simplifies operations by providing centralized control: your finance and tech teams manage one system with consolidated reporting, instead of juggling multiple PSP dashboards.

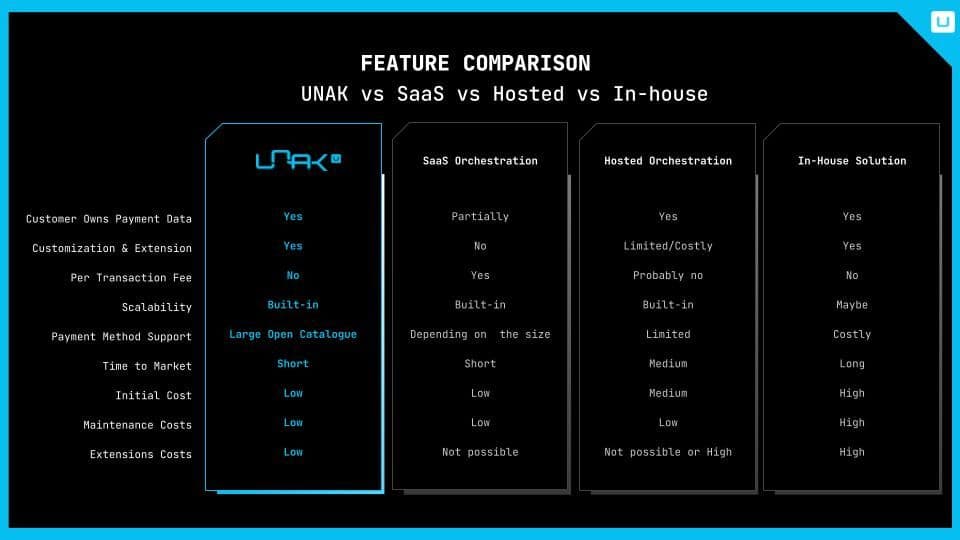

SaaS vs. In-House vs. White-Label Orchestration Solutions

When choosing a payment orchestration platform, businesses have a few deployment options. It’s crucial to understand the differences and pick the model that fits your strategy:

SaaS Orchestration Platforms: These are cloud-based services offered by third-party providers on a subscription or usage-based model. A SaaS (Software-as-a-Service) orchestration platform is typically hosted and maintained by the vendor – you simply integrate via APIs. Pros: Quick to implement (one integration gives access to many connectors), no infrastructure to manage, and you benefit from ongoing feature updates. Cons: Transaction fees or revenue sharing may apply, and you have less control over customization. Examples include Primer and Spreedly, which offer a single API to hundreds of gateways worldwide. These are great for merchants who want speed and ease without heavy upfront investment.

In-House (Built or Self-Hosted) Orchestration: In-house means you develop or deploy the platform within your own environment. Large enterprises with sufficient resources sometimes build their own orchestration layer or use a provider’s software deployed on-premises. Pros: Maximum control over features, data, and costs (no per-transaction fees to an outside orchestrator). You can tailor the system to your specific business flows and keep sensitive data within your security perimeter. Cons: High development and maintenance effort, longer time to market, and you’ll need dedicated expertise to handle compliance (PCI DSS, etc.). This approach is often taken by very large merchants or fintech companies for whom payments are a core competitive advantage (for example, a global e-commerce giant might build an in-house orchestration to connect directly to banks and networks).

White-Label Orchestration Solutions: A white-label platform is a ready-made orchestration software that you can license and brand as your own. It’s essentially a hybrid approach – you get a fully developed platform (often available for on-premise or private cloud deployment) from a vendor, but you run it under your brand. Pros: Faster than building from scratch, yet you maintain ownership of the infrastructure and can customize the branding and sometimes features. It’s popular with payment companies (like ISOs, payment facilitators, or even banks) that want to offer orchestration to their clients without developing the tech in-house. Cons: It may require a significant license fee or revenue share, and you rely on the vendor for major upgrades. Examples of white-label payment orchestration providers include Akurateco and IXOPAY, which offer their platform software with the ability to customize and even resell it. One such platform, Magnius, is explicitly described as a white-label payment gateway suitable for banks, PSPs, and merchants – allowing full custom branding but with the complexity of setup as a trade-off.

In summary, SaaS is ideal for merchants who want a turnkey solution quickly, in-house is suited for those who have unique needs or scale that justify heavy investment (common in large enterprises or tech-savvy organizations), and white-label is great for companies that themselves operate in payments (or large merchants) looking for a middle ground of control and speed.

Standard Components and Features of a Payment Orchestration Platform

Regardless of the model, most robust payment orchestration platforms share a set of core components that enable their functionality:

Smart Routing Engine: The brain that decides where to send each transaction. It evaluates factors like payment type, currency, amount, and real-time performance data to route the payment to the best provider (gateway or acquirer) for authorization. This engine often includes cascading logic – if the first attempt is declined or times out, the transaction is automatically tried through an alternative path. By finding the optimal route for each payment, the platform improves success rates and reduces costs.

Payment Tokenization Vault: A secure vault for storing customers’ sensitive payment data (card numbers, bank account details, etc.) and converting them into tokens. Tokenization allows merchants to offer one-click checkout and subscription services securely. The orchestration platform’s vault is typically PCI DSS compliant, meaning the merchant offloads much of the data security burden. Tokens are usually universal within the platform, so if you switch back-end processors, the same token can be used across different PSPs – preventing vendor lock-in of your customer data.

3-D Secure (3DS) and Authentication Module: To combat fraud and meet regulatory requirements like PSD2 SCA in Europe, orchestration platforms incorporate 3DS authentication flows. The platform will trigger a 3DS check (for example, redirecting to the issuing bank’s verification page or an embedded 3DS flow) when required, working with services like Visa Secure or Mastercard Identity Check. By handling authentication within the orchestration layer, merchants ensure compliance without integrating yet another separate solution. This module often works hand-in-hand with fraud rules – e.g. skipping 3DS for low-risk transactions or applying it based on amount thresholds.

Fraud Prevention & Risk Management: While some merchants use a standalone fraud service, many orchestration platforms either include an integrated fraud screening tool or allow easy integration of third-party fraud systems. The platform can funnel transactions through fraud checks (device fingerprinting, velocity checks, blacklists, machine-learning scoring, etc.) before or during the authorization process. A key benefit is the ability to orchestrate multiple fraud providers or customize rules per region/product – all managed centrally. This reduces fraud losses and can improve approval rates by tailoring risk checks (for instance, being more lenient with trusted returning customers to avoid false declines).

Subscription and Recurring Billing: For businesses that have recurring revenue (subscriptions, memberships, installments), the orchestration platform often provides a subscription management module. This handles storing payment tokens with consent for recurring charges, automating charge schedules, retrying failed subscription payments, sending reminders/notifications, and proration or upgrades/downgrades if needed. Instead of integrating a separate billing system, the merchant can manage subscriptions natively in their payment hub, which simplifies operations for SaaS and subscription-box models.

Ledger and Reconciliation System: A built-in transaction ledger records all payment events (authorizations, captures, refunds, chargebacks) in detail. This serves as an internal source-of-truth for finance teams. Additionally, orchestration platforms can automate reconciliation – matching incoming settlement deposits from various acquirers against the transactions in the system. Because all transactions across providers flow through one platform, reconciliation can be unified and even real-time, saving enormous manual effort. For example, instead of your accountants logging into five PSP portals and dealing with different report formats, the orchestration software aggregates all that data and can output a single, standardized report or feed into your ERP. This greatly reduces human error and delays in financial reporting.

Dashboard and Analytics: A user-friendly admin interface where business and ops teams can monitor transactions across all providers, analyze performance, and configure rules. From one dashboard, you might turn payment methods on/off, switch routing priorities, or set up A/B tests for routing. The platform also provides analytics on approval rates, transaction costs, provider performance, etc., often in real time. This insight helps merchants make data-driven decisions – for instance, identifying that Gateway A has higher decline rates in Brazil at night, so you re-route nightly Brazilian traffic to Gateway B. Having comprehensive data in one place is a major advantage of orchestration.

Integrations Catalog: Modern orchestration solutions pride themselves on offering a large library of pre-built integrations – not only to PSPs and gateways globally, but also to value-added services: fraud tools, identity verification services, loyalty programs, accounting software, alternative payment methods (like PayPal, Alipay, Klarna), and more. A strong platform might have dozens or even hundreds of such connectors available. For example, one leading SaaS POP (Payment Orchestration Platform) connects merchants to 120+ payment gateways/PSPs and 100+ payment services out-of-the-box. This “app store” approach means a merchant can quickly enable new payment methods or capabilities via configuration instead of heavy development.

(Note: Some platforms may use different terminology or bundle these functionalities differently, but the above covers the typical components.)

Choosing the Right Orchestration Platform for Your Business

Not every business has the exact same needs. One of the key tasks for decision-makers is to align the platform choice with company size, transaction volume, technical capacity, and strategic goals:

Small-to-Medium Businesses (SMBs) and Startups: If you’re an emerging merchant primarily operating in one region, you might currently rely on a single payment gateway (e.g., just Stripe or PayPal). As you grow, signs that you need orchestration include expanding internationally, adding new payment options, or seeing a plateau in authorization rates. For SMBs, a SaaS orchestration platform is often the best choice – it minimizes upfront cost and technical overhead. You get access to a broad range of payment methods (helping you localize payments as you expand) and features like tokenization and 3DS without building them yourself. Look for providers that charge a modest monthly fee or a small fee per transaction, and consider those with strong support and documentation (since smaller teams might need more guidance). Example: A midsize e-commerce retailer in Europe might use an orchestration SaaS to easily add local payment methods like iDEAL or Bancontact and improve conversions in those markets.

Large Enterprises: Enterprises operating at scale – think major retail chains, marketplaces, travel companies, or digital giants – will benefit enormously from payment orchestration, but they also demand more control. These companies often have millions of transactions per month and a presence in many countries. For them, the cost of payment failures or suboptimal routing is very high, so an orchestration platform that they can finely tune is key. Enterprises may opt for a self-hosted or white-label orchestration solution to keep everything in-house. The absence of per-transaction fees can save a ton once transaction volumes are large (for instance, a company processing $500M annually might prefer a fixed-cost platform in-house, avoiding a few basis points on each transaction). Additionally, owning the infrastructure allows integration with internal systems (like linking the orchestration platform directly to the company’s data warehouse, CRM, or custom fraud models). Example: A global streaming service might deploy a white-label orchestration platform on its own cloud, giving it the flexibility to route payments via regional acquirers and store all payment data internally for analysis.

Payment Service Providers and Fintechs: Interestingly, payment orchestration isn’t just for merchants – banks, acquirers, and fintech companies themselves use white-label orchestration to enhance their offerings. A regional PSP could license an orchestration platform to quickly provide connections to more payment methods and geographies to its merchant clients. In this case, the PSP becomes the provider of the orchestration (under their brand), which is a faster go-to-market than building from zero. If you are a fintech or ISO looking to offer merchants a full payment hub, a white-label orchestration solution can be your backbone. Ensure the platform is modular (so you can offer or restrict features per your business model) and check that it’s PCI compliant and secure since you’ll be handling many clients’ transactions.

In all cases, when evaluating a payment orchestration platform, consider the breadth of integrations, reliability and uptime, pricing model, compliance certifications (PCI DSS Level 1 is a must), and how easily it scales. Also, look for case studies or examples in your industry – for instance, if you’re in travel, does the platform have features for multi-currency and high-value ticketing transactions? If in subscription business, does it natively handle recurring billing quirks?

Examples of Leading Orchestration Platforms

To put things into perspective, here are a few well-known payment orchestration platforms and what types of businesses they suit:

Spreedly: A pure-play payments orchestration API known for its extensive integrations (120+ payment gateways). Spreedly is a SaaS platform – you integrate once and can transacting through a global network. It’s popular among SaaS platforms and marketplaces that need to work with multiple PSPs. Use case: An online marketplace connecting buyers and sellers globally can use Spreedly to quickly add regional payment options without individual integrations.

Checkout.com’s Orchestra (hypothetical): (For illustration) A large PSP like Checkout.com provides its own orchestration layer for enterprise clients, combining gateway and orchestration features. This could be ideal for enterprise retailers who want a one-stop solution but still multi-acquirer capability.

Akurateco: An Amsterdam-based white-label payment software provider. It offers a SaaS platform with 300+ connectors and focuses on smart routing and cascading to improve conversion. They highlight up to 30% increase in conversion with cascading and robust real-time analytics. Use case: Mid-to-large merchants or even smaller payment providers wanting a ready-made platform to host themselves and brand it.

IXOPAY: An independent orchestration platform that provides a white-label gateway with multi-acquirer support and rich features like risk management, routing, and reconciliation. It’s designed to be easily integrated into existing systems (offering plugins, SDKs, API, etc.). Use case: Enterprises or payment facilitators that need an orchestration engine with a friendly interface to manage complex payment flows.

UNAK: Best of both world - Its open architecture, with no transaction fee, full control of data & scalability, and with standart implementation +150 connectors ready to help you optimize your work and budget.

Each of these caters to slightly different audiences (some more to merchants, some to other providers). The good news is that the market is quite mature in 2025, with many providers to choose from. This competition means you can likely find a platform that matches your business size and needs closely – whether you prioritize cost, ease of use, or maximum control.

Outcome

A payment orchestration platform is increasingly a must-have for enterprise merchants and ambitious online businesses. It is the technology answer to an overly complex payments landscape. By centralizing payment channels and providers, it empowers businesses to boost conversion, cut costs, and streamline operations all at once. Instead of being locked into one payment gateway’s limitations, merchants can be agile – adding new payment methods on the fly, switching providers when advantageous, and ensuring customers always have a seamless experience.

When implemented correctly, payment orchestration becomes a strategic asset: your payments no longer just “work,” they work smarter and harder for your business. As you consider the options (SaaS vs in-house, etc.), keep in mind your long-term growth. The right platform will scale with you, opening doors to new markets and opportunities. In the following parts of this series, we’ll dive deeper into how these platforms function internally, how they solve global payment challenges, and how you can maximize their value.

Share:

Qaiware

Payment solution expert

OVER 15+ YEARS WE ARE BUILDING COMPLEX PAYMENT PRODUCTS FOR BLUE CHIP CLIENTS