Insights

Digital Payment Hub: Payment Orchestration Platform

POP as a Digital Payment Hub: Unifying Payment Systems with Open Architecture

In the context of payment orchestration, POP stands for Payment Orchestration Platform. In this part of our series, we examine how a POP can serve as a digital payment hub for an enterprise – essentially becoming the central node through which all payment-related activities and systems connect. We’ll highlight the importance of an open architecture, the ability to plug in third-party modules, and how some businesses are even opting for self-managed orchestration to gain ultimate control.

Think of a digital payment hub as the mission control for everything related to payments: not only processing transactions, but also linking to fraud prevention, accounting, analytics, customer management, and more. Traditionally, large organizations might have separate systems for each of these, leading to silos and integration pain. A modern POP, however, is built to integrate and orchestrate beyond just payments – it fosters an ecosystem.

From Orchestration Layer to Central Hub

Payment orchestration’s evolution: Initially, payment orchestration was about connecting multiple PSPs and gateways to optimize transactions (what we covered in previous sections). As the technology matured, these platforms recognized they sit at a strategic junction of data and processes, which means they can expand their role. Today’s leading POPs aim to be a one-stop platform where merchants can manage not only the flow of payments but all the ancillary services around payments.

For example, instead of logging into one system for payments, another for chargeback management, and a third for analytics, the orchestrator can either provide these features or integrate them so that the merchant accesses everything through the orchestration hub. This “hub” approach provides a single source of truth and a single control point.

Connecting All Payment-Related Systems Under One Roof

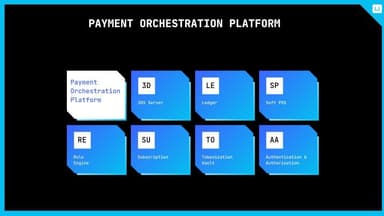

A digital payment hub centralizes connections to all the systems and service providers that touch the payment lifecycle:

Multiple PSPs/Acquirers: As expected, it connects to various payment processors and gateways (credit card acquirers, alternative payment method providers, etc.). This covers the core processing of transactions. Instead of your system integrating with each provider, the hub integrates with all and you integrate just with the hub.

Alternative Payment Methods (APMs): These include mobile wallets, bank transfer schemes, buy-now-pay-later providers, etc. A payment hub ensures new popular methods can be onboarded easily. For instance, if you want to add PayPal, Amazon Pay, Klarna, and Apple Pay – a hub likely has standardized modules for each. You enable them, and now they’re part of your payment ecosystem, feeding data into the same hub and managed alongside cards.

Fraud and Risk Tools: Many companies use third-party fraud prevention services or proprietary risk engines. A robust POP can integrate these in a couple of ways: The benefit is that even if you use multiple fraud solutions (some companies layer them), the orchestration hub can aggregate their outputs and help you manage them in one place. It’s an open ecosystem approach – use whichever fraud tool is best, plug it into the hub’s workflow. For example, UNAK (Qaiware’s orchestration software) boasts an open catalogue of integrations extendible to anyone, covering payment processors and also risk and fraud providers. That means merchants aren’t limited to the hub’s native fraud tool; they can plug in any vendor of choice into the ecosystem.

Natively: It might come with a built-in rules engine or ML fraud detection.

Third-party module integration: Through APIs, it can route transactions to an external fraud service (like ThreatMetrix, ClearSale, Riskified, etc.) and get a risk decision, then continue the flow. In a hub, the result of a fraud check (approve/deny or a risk score) can be used to orchestrate the next steps (e.g., if a high risk score, don’t send to authorization and instead decline).

3DS Servers and Authentication services: As part of security, if you want to use a specific 3-D Secure provider (maybe your bank has one, or a third-party like CardinalCommerce), the open hub can integrate that. Some merchants in high-risk sectors also use identity verification (KYC) services on the fly – those too can be integrated. The hub orchestrates the sequence: verify identity -> then authorize payment, for instance.

Core Business Systems (ERP, CRM, etc.): A big advantage of a self-managed orchestration hub is you can connect it deeply with your internal systems. For example, integrate your ERP/Accounting system so that when transactions settle, the data flows into your financial ledgers automatically. Or connect your CRM, so that customer payment events update their profile (like purchase history, loyalty point triggers, etc.). Because the hub has all the payment data and outcomes, linking it to these systems means they all get real-time updates. In open architectures, APIs or webhooks make this feasible; the orchestration platform might expose webhooks for every event (payment succeeded, failed, chargeback filed, etc.) that you can subscribe to and update your other systems.

Data Warehouses and Analytics Tools: Enterprises often pipe data to a central data warehouse or use analytics/BI tools (like Tableau, PowerBI). A payment hub can directly feed into those with unified data. Some orchestration platforms also have their own analytics dashboards, offering insights like conversion funnels, provider comparisons, geographic performance and so on. But if you have a custom analytics stack, you can export the data or query it from the hub. The key is that data isn’t trapped in different silos – all payment events and related info (like fraud scores, method used, etc.) aggregate in one dataset.

Chargeback Management Systems: Handling disputes and chargebacks can be a separate workflow. Many merchants use outsourced chargeback services or software. The payment hub can integrate with those as well: for instance, when a chargeback is received from an acquirer, the orchestration platform logs it and can send the details to your chargeback management tool, or even trigger automated responses. Conversely, if your CRM or support resolves something and you want to issue a refund to avoid a chargeback, doing it through the hub ensures it updates across systems.

Payout Systems: If you also disburse funds (like a marketplace paying out to sellers, or a gig platform paying contractors), an orchestration hub can manage outbound payments too. Many POPs now include payout capabilities connecting to things like bank transfer networks, PayPal MassPay, push-to-card, etc. By treating payouts as part of the ecosystem, the hub covers the full cycle of money movement.

Essentially, a digital payment hub turns a web of individual connections into a single, cohesive network managed via the orchestration platform. This simplifies architecture enormously for an enterprise. It also reduces duplicated integrations – rather than your IT team writing separate code for each new provider or tool, you integrate once with the hub and just configure the new service within it.

The Power of Open Architecture

A term that comes up often is “open architecture.” In the context of payment orchestration, an open architecture implies:

The platform is agnostic and vendor-neutral (it’s not forcing you to use only certain providers).

It offers open APIs and possibly even SDKs or modules for developers to build on or integrate new things.

It supports a plugin model or at least flexible integrations, allowing third parties (or your own developers) to extend it.

For example, UNAK’s platform is described as being built on an agnostic, open architecture with an “unprecedented open ecosystem”. This suggests that anyone (with the right access) can integrate new payment methods or services into UNAK without waiting on the vendor’s proprietary development. It’s more like a framework than a closed SaaS product.

Why does open architecture matter? Because it future-proofs your payments hub. New FinTech innovations emerge all the time – a new payment method, a new risk scoring AI, etc. If your orchestration hub is open, you can plug these in as they become relevant. You’re not stuck with only what the platform vendor supports. This is particularly important for enterprise merchants who might have custom needs. For instance, maybe you have a unique loyalty points payment option you offer customers – you can integrate that into the hub’s checkout logic if the platform is extensible.

Open architecture also means data portability and ownership. You have access to your data through open channels (APIs). You’re not locked out of any functionality because of closed systems. If needed, you could even build bespoke modules. Some orchestration platforms might allow custom code or scripts for handling specific logic in the flow.

Analogy: Think of a smartphone with a closed OS vs. an open one. A closed system only lets you use built-in apps; an open system allows third-party apps, so the device can do a lot more. Similarly, an open payment hub allows third-party “apps” in the payments flow (fraud checks, analytics, payment connectors, etc.).

Another aspect is community and ecosystem: Certain orchestration providers foster a community where partners build integrations (like how there are app stores or marketplaces). This can accelerate innovation. For example, if there’s demand for a new payment method in a region, perhaps a third-party or the payment method provider can build the integration plugin and offer it via the platform’s ecosystem, rather than the platform provider having to do all development.

For enterprises, open architecture also can mean the difference between having to adapt your business to the software versus the software adapting to your business. No one wants to be constrained in how they serve their customers due to a platform’s limitations.

Third-Party Modules and a Modular Approach

Building on open architecture, the modular design of a payment hub is key. A modular payment orchestration platform means you can use the components you need and perhaps skip or swap those you don’t:

For example, if you love everything about a POP’s capabilities but prefer to use your own fraud system instead of the built-in one, a modular platform would let you disable its fraud module and plug yours in.

Or if you start with basic needs and later want to add, say, a currency conversion module or a payout module, you can do so without a complete system overhaul.

Some providers might even let you license modules separately (especially in white-label scenarios for banks/PSPs, they might pick and choose modules like “Gateway module”, “Fraud module”, etc.).

Third-party modules could refer to add-ons developed outside the core platform that you can integrate. This could include:

A specific fraud detection module by a specialist vendor.

An advanced analytics or AI module that, for instance, analyzes decline reasons and suggests optimizations (something a consultancy might plug in).

Industry-specific modules, e.g., a module for travel merchants that integrates with industry systems like BSP (Billing and Settlement Plan) – not standard in all POPs, but a third party could make one to extend an open platform for travel industry needs.

The presence of third-party modules indicates a healthy ecosystem. It also often correlates with white-labeling and self-management: if a platform is offering itself as a toolkit for others (like banks or payment companies), it usually is modular.

Self-Managed Orchestration – Taking Control In-House

“Self-managed orchestration” means the merchant or an intermediary hosts and runs the orchestration platform themselves, rather than using it as a cloud service. This typically goes hand-in-hand with open architecture because you need that flexibility to run it on your own.

Why would a merchant want to self-manage an orchestration platform? There are a few compelling reasons for some:

Cost Efficiency at Scale: As mentioned, removing volume-based fees is a big driver. If you run the platform in-house (perhaps paying a license or having built it), you aren’t paying per-transaction fees to an orchestration provider. Merchants doing tens of millions of transactions can save significantly this way, even after accounting for hosting and support costs.

Full Data Ownership: When self-hosted, absolutely all payments data and customer information resides in your databases (or cloud) under your control. For highly regulated or sensitive industries, this is attractive. It also makes internal integrations easier because everything is within your network.

Customization: Self-managing means you can customize the platform’s behavior to a fine degree. Want a very custom routing algorithm? If you have the source or extension capabilities, you can implement it. Want the UI of the dashboard to reflect your company’s terminology or to integrate with your login SSO? You can often do that with self-hosted since you have access to the system itself.

No Vendor Constraints: If the orchestration provider goes out of business or changes policies, a self-hosted solution insulates you. You have the platform running regardless. Essentially, you’re treating the orchestration platform like a core part of your infrastructure (akin to how some companies use open-source software internally for crucial tasks).

However, self-managed is not for everyone – it requires tech expertise and resources to maintain. That’s why some merchants opt for it only when they reach a scale where the benefits clearly outweigh the effort.

UNAK (by Qaiware) is an example of a platform offering this approach. It’s described as modular software that “brings PSP and orchestration functionality in-house” and imposes no transaction fees or limits, offering full ownership. They highlight that it “offers full ownership and control of valuable payment data” and “a modern technological setup that can easily scale and adapt, while leveraging commoditized solutions”. These points appeal to enterprises that want their payment hub to be an internal asset. Essentially, Qaiware built UNAK so companies could run their own digital payment hub with an open ecosystem – aligning perfectly with what we’re discussing.

The combination of open architecture + self-management can revolutionize how an enterprise perceives its payments infrastructure. It’s no longer seen as an external service or a cost center, but rather as a customizable platform akin to how they might view their own website or app backend – something they can continuously innovate on.

Benefits of a Payment Hub Approach

To summarize the key benefits an enterprise gets by using a POP as a digital payment hub with open, modular architecture:

Holistic View of Payments: All channels, all methods, and all ancillary services feed into one platform. This gives unprecedented visibility (for example, a single customer view of their purchases across web, mobile, and in-store, all in one timeline).

Simplified Operations: Managing integrations, security compliance, and vendor relationships becomes simpler. Your tech team handles one system, your ops team uses one dashboard. Training, maintenance, and updates are more straightforward than juggling many independent systems.

Flexibility and Innovation: You can quickly adopt new technologies (via third-party modules or new integrations) without waiting years for an old system to support it. If cryptocurrency payments suddenly become important, an open hub could allow adding a crypto processor integration swiftly. If a regulatory change happens, you can adapt rules in the hub rather than rewriting multiple systems.

Scalability: As your business grows in volume or complexity, the hub scales with you. Need to add 5 new payment methods or double the transaction load? A well-architected hub (especially self-hosted on cloud infrastructure) can scale horizontally to meet demand. The modular design also means you can distribute load (maybe have separate instances handling different regions but all under one logical hub).

Vendor Independence: You aren’t tied to any single provider or tool. If one component underperforms, swap it out. For example, unhappy with Fraud Service A? Plug in Fraud Service B. Gateway raising fees? Add another gateway and shift traffic. The hub orchestrates, so switching costs are lower. This competitive freedom often yields better pricing and service from vendors (since they know you can switch).

Use Case Expansion: With a versatile payment hub, you can enable new business models. Want to become a marketplace? The hub can handle splitting payments and payouts to vendors. Want to launch a subscription service in addition to one-off sales? The hub supports both simultaneously. It’s easier to experiment with new revenue streams when your payment infrastructure is not a limiting factor.

A practical example: A large online marketplace used an orchestration platform as a hub not only to route payments but to integrate their storefront platform, their inventory system, and their customer support system. When a payment failed due to a bank issue, the hub triggered a notification in the customer support interface so the support team could proactively reach out to the customer and assist. It also updated the order status in the inventory system (to not ship until payment confirmed). This kind of cross-system automation would be very hard without a central orchestrator coordinating and communicating with all parts.

Insights

By leveraging a Payment Orchestration Platform as a digital payment hub, enterprises effectively create an open payments ecosystem tailor-fit to their needs. This hub is more than just a transaction processor – it’s the integration point for every payment and financial tool in the business. With open architecture, the platform becomes a living system that can evolve with the business, absorbing new technologies and processes instead of being disrupted by them.

For decision-makers, adopting a payment hub approach means investing in a flexible infrastructure rather than piecemeal solutions. It’s a strategic shift: treating payments as a central platform (often an in-house asset) rather than a peripheral service. The payoff is long-term agility, cost savings, and the ability to deliver a consistent, excellent payment experience to customers across all channels and markets.

In the next article, we’ll provide a guide for merchants on payment orchestration – a more hands-on overview geared towards business leaders on how to get started with orchestration and make it successful.

Share:

Qaiware

Payment solution expert

OVER 15+ YEARS WE ARE BUILDING COMPLEX PAYMENT PRODUCTS FOR BLUE CHIP CLIENTS