Insights

Payment Orchestration Guide for Merchants

Payment Orchestration Guide for Merchants: Benefits and Implementation Steps

Payment orchestration might sound technical, but for merchants it boils down to a simple promise: make payments easier, smarter, and more profitable for your business. This guide will walk through what payment orchestration means in practical terms for merchants, the key benefits you can expect, and how to implement it effectively. We’ll keep the language business-friendly and focus on how orchestration solves real problems merchants face every day.

What is Payment Orchestration? (A Merchant-Friendly Definition)

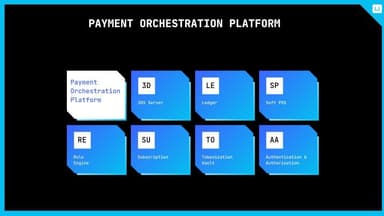

Payment orchestration is essentially a master system for payments. Instead of using one payment provider here, another tool there – you have a single platform that connects to all your payment methods and services and lets you manage them together. Think of it as hiring a payment “maestro” for your business: this maestro coordinates between the banks, credit card companies, wallets, fraud checkers, etc., to ensure every customer’s payment can go through in the best way possible.

From a merchant perspective, when you use a payment orchestration platform:

You integrate your website or app to one platform (the orchestrator), and it’s already connected to many payment providers (Visa, MasterCard, PayPal, Stripe, local banks, etc.).

In your day-to-day, you operate in one dashboard – viewing all transactions and controlling settings centrally.

The platform handles the heavy work of routing payments, securing data, and dealing with multiple banks so you don’t have to do it manually.

A simple analogy: Without orchestration, if you wanted to accept 5 different payment types, it’s like maintaining 5 separate terminals/systems. With orchestration, you have one smart terminal that accepts all 5 and optimizes each transaction behind the scenes.

Why Merchants Should Care: Key Benefits at a Glance

Adopting payment orchestration can deliver several concrete benefits for your business. Here are the major ones in business terms:

Higher Sales Conversion: More payments approved = more revenue. An orchestration platform intelligently routes each payment to maximize the chance it’s approved (for instance, if one bank declines a card, it can try another route automatically). Also, by offering more payment options (credit cards, debit, e-wallets, buy-now-pay-later, etc.), you cater to customer preferences, which means fewer abandoned carts. In fact, giving customers their preferred payment method has been shown to significantly increase conversion rates and reduce cart abandonment. Orchestration ensures you can offer those options without headache.

Lower Payment Processing Costs: This happens in a couple of ways. The platform can route transactions in a cost-efficient manner (e.g., using a lower-cost provider when possible). It also enables you to avoid unnecessary fees – for example, if you use one provider for everything, you might be paying high cross-border fees or a premium for convenience; orchestration lets you shop around per transaction automatically. Over time, these savings add up. Some merchants have saved on transaction fees by introducing multiple providers and letting the orchestrator send payments to the cheapest option available each time. Also, if you handle enough volume, orchestration allows you to negotiate better rates with multiple processors and not be stuck with a single vendor’s prices.

Improved Checkout Experience: A seamless payment experience keeps customers happy and loyal. Orchestration helps by: All these lead to higher customer satisfaction and repeat purchases. When payments “just work” quickly, customers trust your site more.

Ensuring your checkout rarely has errors or downtime (because if one payment partner has an issue, the orchestrator can failover to another).

Letting you offer local payment methods in international markets easily – customers feel at home when they see familiar options (like Alipay in China, or Klarna in Europe).

Enabling features like one-click checkout or saved payment details securely through tokenization. Customers don’t have to re-enter info every time, which makes purchasing frictionless.

Simplified Operations and Reporting: If you’ve been selling through multiple channels or using different payment gateways, you know how painful reconciliation and reporting can be. Each system has its own report – you spend time merging data to see the full picture. With orchestration, you get one unified report/dashboard. You can see total sales, broken down by payment method or region or provider, all in one place. Refunds and chargebacks processed through the platform also reflect in one system. This not only saves a ton of staff hours but also reduces errors. Your finance team will thank you for not having to cobble together spreadsheets from various sources.

Easier Expansion to New Markets: Planning to go international or launch in a new region? Payment orchestration greases the wheels. Since the platform likely has integrations in many countries, you can quickly enable the payment methods popular in the new market. For instance, expanding to Asia? The platform may support Alipay, WeChat Pay, UnionPay, etc. You toggle them on and have local payment acceptance from day one. Additionally, the platform deals with currency conversion and local banking relationships, meaning you don’t necessarily need a local entity or bank account right away to start selling. This fast-tracks your go-live in new markets. Merchants who used to spend 6 months setting up payments in a country can do it in a few weeks with the right orchestration provider.

Better Risk Management: Fraud and chargebacks can eat into profits and overhead. Orchestration platforms often come with built-in fraud prevention or easy integration to third-party tools. By centralizing this, you ensure every transaction is screened properly, and you can apply consistent fraud rules across all sales channels. This reduces fraudulent orders slipping through and likewise avoids unnecessarily rejecting real customers (false positives) because the system gets smarter with centralized data. Also, with features like 3-D Secure 2.0 integrated, you can shift liability on fraud-related chargebacks back to issuers for card payments (after successful authentication), protecting you from those losses. In short, you can expect lower fraud losses and lower chargeback rates when using orchestration effectively – or at least, you can handle the same with less manual work.

Full Control and Flexibility: Perhaps one of the less tangible but important benefits: you regain control of your payments strategy. Instead of being locked into one provider’s roadmap or terms, you have the flexibility to switch or add providers as your business dictates. Running a holiday promotion and worried your main gateway might throttle under volume? Add a backup provider via the orchestration platform as insurance. Want to try a new payment method like a cryptocurrency option? See if the platform supports an integration and pilot it without disrupting your whole checkout. This agility means you can respond faster to business needs or customer trends, gaining a competitive edge.

To summarize in a merchant-centric way: payment orchestration helps you sell more, spend less on fees, and sleep better knowing your payments are under control. It turns the chaos of multiple payment methods and providers into a well-oiled, manageable system.

Signs You’re Ready for Orchestration

How do you know if your business should seriously consider a payment orchestration solution? Here are some common triggers:

You’re operating in or expanding to multiple countries and facing complexity in accepting local payment methods or dealing with currency issues.

You have or plan to have multiple payment providers (gateways, processors) and it’s becoming a lot to manage or isn’t optimized (maybe you added a second one for redundancy or region, but switching between them is manual).

Your authorization rates (approval rates) are not as high as you’d like, or you suspect they could be higher – maybe you see certain declines you think could be saved.

Payment-related IT work consumes too much time (integrating new methods, maintaining PCI compliance, etc.), delaying other projects.

Customers or internal stakeholders are asking for payment options or reports that are hard to provide with your current setup (e.g., “Can we see all PayPal and credit card sales in one view by region?” or “Can we add Apple Pay quickly?”).

You’re concerned about uptime – perhaps you’ve had an incident where your single payment gateway went down and sales stopped. That risk is prompting you to add resilience.

If any of these resonate, orchestration is likely the path forward.

Implementing Payment Orchestration: A Step-by-Step Guide

Implementing an orchestration platform can be straightforward, but like any significant change, it helps to approach it methodically. Here’s a practical step-by-step approach:

Assess Your Needs and Goals: Start by clearly identifying what you want to achieve with orchestration. Is it to improve approval rates? To cut costs? To expand payment options? And what’s your current payment setup? Make a list of the payment methods and providers you use, your average transaction volumes, pain points (e.g., “spending X hours on reconciliation weekly” or “losing Y% transactions to declines”). This will help you choose the right platform and configure it properly.

Research and Choose a Platform: Look for payment orchestration providers that cater to your business size and industry. Some platforms specialize in enterprise, some in mid-market, etc. Key factors to consider: It’s a good idea to involve both technical team members (to evaluate integration effort) and business stakeholders (to evaluate features and ROI) in this decision. Many providers will offer demos or even a sandbox for testing.

Does it support all the payment methods you need (or plan to need soon)?

Does it easily integrate with your sales channels (does it have good APIs, support popular e-commerce platforms if applicable, etc.)?

Pricing model – is it volume-based, flat, or something else? Make sure it makes financial sense given your transaction count.

Performance and reliability – any references or case studies? (e.g., Platform X helped merchant Y raise approval by 5%, or they have 99.99% uptime guarantee).

Features – like built-in vault, fraud tool, subscription handling if you need recurring, etc.

Support and onboarding – will they assist with migration and are they known for good support?

Plan the Integration and Migration: Once you’ve selected a platform, plan out the implementation. This includes:

Integration approach: How will you connect your website/app to the new platform? This usually means using their API or SDK. If you have an existing payment module in your app, you might need to replace or modify it to point to the orchestrator. The provider’s tech team often helps with this architecture.

Data migration: If you have stored customer payment data (tokens) with an old provider and you want to migrate those to the orchestration platform’s vault, coordinate this. Good orchestration providers have procedures for secure token migration (so customers don’t have to re-enter cards). It might involve the old provider sharing encrypted card info or mapping their tokens to new tokens.

Phased rollout: Decide if you’ll do a big switch or gradual. Many merchants do a phased approach: route a small percentage of traffic through the new platform initially (while the rest still goes the old way) to monitor performance, then increase it. Or you might move one country or one brand at a time if you operate several.

Testing: Set up a testing environment and run a variety of payment scenarios through the orchestration platform before going live. Test different payment methods, declines, 3DS flows, refunds, etc. This ensures your team is familiar with how everything appears in the new dashboard and that your integration is solid.

Team Training and Process Update: Train your relevant teams on the new system:

The finance and operations folks should learn how to use the orchestration dashboard for reconciliation, reporting, and manual actions (like issuing refunds).

Customer service should be aware of the new system, especially if the interface for looking up transactions changes. They’ll need to know how to quickly find a customer’s payment and status in case of inquiries.

Technical team should know how to monitor the integration in production and who to contact for support if issues arise. Additionally, update any internal process documentation. For example, if previously you reconciled via a certain report from your gateway, now it will be via the orchestration platform’s reports – note those changes in your SOPs.

Go Live and Monitor: Launch the orchestration platform connection in production (either fully or phased as per your plan). In the initial days/weeks, closely monitor: Many providers will have someone check in with you during this period to help tweak settings or address any anomalies.

Transaction success rates, comparing with previous baseline. Are more transactions getting approved? (Hopefully yes – even early on you might see improvement as the platform might route better).

Any errors or failures – check logs and the platform’s dashboard for any failed transactions and investigate if they’re due to integration issues or genuine declines.

Customer feedback – are customers experiencing any confusion or issues at checkout? Ideally they shouldn’t notice anything except possibly more payment options. If you added new methods, is adoption growing?

Financial settlement – ensure that funds from the new flows are being deposited as expected and match the reports, so you can trust the reconciliation.

Optimize and Expand: Once stable, you can start leveraging the orchestration platform to its fullest: Essentially, treat this platform as an ongoing tool – it’s not a “set and forget.” The more actively you manage and optimize with it, the bigger the gains. Many merchants even dedicate someone as a “payments optimizer” role to continually refine things in the orchestration system.

Turn on additional payment methods that you were not offering before, to see if they boost conversion in certain markets.

Experiment with routing rules. For example, you might A/B test two acquirers to see which gives better approval rates and then adjust your default routing to favor the better one. The platform’s analytics can guide this – some have features to automatically choose the best route or you can set your own rules like “Use Provider A unless decline, then Provider B.”

Use the data insights to spot trends. Perhaps you find that transactions above $500 have lower approval – you might then implement 3DS for those via the platform to see if that helps (or route high-value transactions to a provider known for handling those well).

If you’re in a subscription business, monitor how the retry logic is recovering failed renewals. Tweak the retry intervals if needed. Over a few billing cycles, you may notice churn from payment failures drop.

Regularly review cost reports – are you saving money as expected? Maybe you can negotiate down fees with a provider now that volume increased through them via orchestration (since moving to orchestration might allow you to consolidate some volume or move it around).

Leverage Support and Community: Don’t overlook the resources available from the platform provider. They often have other clients with similar setups – they might run user forums or share best practices. If you hit a snag or want to do something new (like adding a certain payment method), reaching out to your provider’s support or account team can accelerate the process. You’re partnering with them to improve your payments; good providers will have a vested interest in your success and may help by analyzing your transaction data and suggesting optimizations (some have consulting as part of enterprise packages).

By following these steps, the transition to an orchestrated payments system can be smooth and yield quick wins.

Real-World Example

To illustrate, let’s take a fictional but representative example: ACME Co., a mid-sized e-commerce retailer that ships globally but is based in the US.

Before orchestration: ACME used a single payment gateway for all card payments and PayPal separately. Their approval rate for international cards was only ~75%. They had frequent complaints of payment failures in Europe and Asia. Also, they only offered USD on their site, so international customers often had to pay in USD (incurring conversion fees on their side).

ACME’s finance team spent a lot of time reconciling PayPal vs card sales and dealing with different reports. They also noticed their payment processing fees were a significant line item, and any negotiation with their single gateway was tough because switching was hard.

After implementing orchestration: ACME integrated a payment orchestration platform. They immediately enabled multi-currency and local routing: now European orders are processed via a European acquirer (through the platform) and Asian orders via an Asia-Pacific gateway that was pre-integrated. They also turned on Alipay and WeChat Pay for Chinese customers and allowed payments in local currency (EUR, GBP, etc.).

Within a month, ACME saw international approval rates rise to ~85% (a big jump in recovered sales). Customers in those regions reported a smoother checkout (no more random declines and they could pay in familiar ways).

ACME’s processing costs per transaction dropped by 10% because the European transactions now avoided cross-border fees and they weren’t solely reliant on one provider’s fees. In fact, their original US gateway even lowered their rates a bit when ACME shifted some volume to others, in order to win some of it back.

The finance team now gets one consolidated report from the orchestration dashboard or API. What used to take half a day of reconciliation now takes an hour. Chargebacks across all methods show up in one feed. They feel far more in control during month-end closes.

When ACME decided to launch in Brazil, they found that the platform had integrations to Boleto (a popular cash voucher in Brazil) and local card processing. They rolled that out in a matter of weeks and had a successful entry to that market, attributing a lot of it to offering local payment options seamlessly.

This kind of story is common – the specifics vary, but merchants large and small have found orchestration platforms to directly boost their top-line (more successful payments) and bottom-line (lower costs, less manual work).

Tips for Success

Ensure Organizational Buy-In: Payment orchestration might be owned by the payments or tech team, but its benefits touch multiple departments (sales, finance, support). Make sure all stakeholders understand the “why” and “how” – it helps to share early wins (like “hey, our approval rate in Canada went up 5% after we switched to orchestration – that’s equivalent to $X extra sales last week!”). This keeps everyone supportive and engaged.

Keep Security in Focus: When implementing any new payment system, confirm the security standards. Use the platform’s hosted fields or tokenization methods so you’re never exposing raw card data. Verify the platform’s PCI compliance (most are Level 1 certified). In short, follow best practices – one advantage is orchestration often simplifies PCI scope for you.

Monitor KPIs Continuously: Define key metrics to watch – e.g., approval rate, processing cost percentage of sales, average days to settle, etc. Monitor these over time via the platform’s analytics or your own tools. This will help you quantify the impact of orchestration and spot if anything starts to dip so you can investigate.

Stay Updated on Features: Providers regularly update their platforms with new integrations or features (like support for a new digital wallet or a new dashboard view). Stay in the loop through their newsletters or account managers. You might find new opportunities to leverage, such as a recently added fraud module or support for a hot new payment app that could give you a marketing edge.

Consider a Backup Strategy: While the orchestration platform gives you redundancy across providers, think about redundancy for the platform itself. This is a single point through which everything flows, so ensure the provider has a strong uptime record and maybe discuss contingency plans (some merchants keep a very basic backup payment flow outside of orchestration in case of an extreme scenario, though top-tier platforms are highly reliable). This is more about risk management culture than an expectation of failure.

By following these best practices, merchants can maximize the benefits of payment orchestration.

Insights

For merchants, a payment orchestration platform is more than just tech jargon – it’s a strategic tool that can directly impact revenue, costs, and customer satisfaction. It brings order and intelligence to what is often a fragmented part of the business.

In summary, payment orchestration will help you:

Increase your approval rates and sales by smartly handling payments (no more unnecessary declines if there’s another way to get it approved).

Delight customers with a smooth, flexible checkout experience featuring their preferred ways to pay.

Save money through optimized fees and streamlined operations.

Empower your team with better data and easier workflows, from finance reconciliation to IT maintenance.

Scale confidently into new markets and channels, knowing your payment infrastructure can handle it.

As a merchant, embracing orchestration is a bit like upgrading from a manual transmission to an automatic, GPS-guided car – you still steer your business, but the platform handles the complex gear shifts and navigation in the background, getting you to your destination faster and with fewer bumps.

Our final installment will compare traditional payment gateways to modern payment orchestration in detail, and show why the latter is increasingly the choice of savvy enterprises (with a look at a solution like UNAK that exemplifies the new breed of orchestration).

Share:

Qaiware

Payment solution expert

OVER 15+ YEARS WE ARE BUILDING COMPLEX PAYMENT PRODUCTS FOR BLUE CHIP CLIENTS