Insights

Payment Orchestration vs. Payment Gateways

Payment Gateways vs. Payment Orchestration: Key Differences and Advantages (UNAK’s Edge)

Merchants often start their journey with a simple payment gateway. As they grow, they hear about “payment orchestration” and wonder: how is it different? Do we need it? In this final article of our series, we’ll compare payment gateways and payment orchestration platforms side by side – covering features, control, scalability, and implementation – to highlight how orchestration provides a more advanced, flexible approach. We’ll also conclude with a look at UNAK, Qaiware’s own payment orchestration software, and its unique advantages for businesses seeking state-of-the-art payments control.

Understanding the Basics: Gateway vs. Orchestration

Payment Gateway: A payment gateway is a service that transmits transaction data from the merchant to the acquiring bank/processor and back. It’s basically the digital equivalent of a point-of-sale terminal. Gateways often come bundled with a merchant account or PSP (Payment Service Provider) services. They typically support a limited set of payment methods (primarily cards, maybe a few alternatives) and focus on securely moving data (handling encryption, connecting to banks). Example: Authorize.net or the gateway service provided by your processor like Stripe or Braintree – you send them the card info, they handle authorization and tell you if it’s approved or declined.

Payment Orchestration Platform (POP): This, as we’ve detailed, is a layer above gateways and processors. It sits between the merchant and multiple payment services, managing and optimizing interactions with all of them. Instead of just moving data for one transaction through one channel, it intelligently routes and directs transactions through potentially multiple channels and adds extra services (routing logic, tokenization, etc.). It’s like having a smart traffic controller for payments – handling many routes and ensuring each car (transaction) finds the best path.

In essence, a gateway is single-channel – it connects you to one processor or network at a time. Orchestration is multi-channel – it connects you to many and decides which to use and when, plus does more than just pass data (it makes decisions, stores data, ensures backup routes, etc.).

Another way to put it: A gateway is a subset component; an orchestration platform might even utilize gateways under the hood but offers a broader solution.

Feature and Capability Comparison

Let’s compare some key aspects:

Connectivity:

Gateway: Connects your site to one acquiring entity (which could be an acquirer or a PSP that in turn connects to many, but from your perspective it’s one). If you want multiple gateways, you integrate each one separately.

Orchestration: Connects to multiple PSPs/gateways/acquirers through one integration. It is designed to manage these multiple connections seamlessly. So one API into the orchestration platform = access to a whole network of providers.

Payment Methods:

Gateway: Usually supports the basics – credit/debit cards for sure, sometimes a couple alternative methods (like maybe PayPal or ACH if the gateway provider added those). But generally limited. If your gateway doesn’t support a method, you’re out of luck or need another integration.

Orchestration: Supports dozens if not hundreds of payment methods by aggregating what all the connected providers offer. One orchestrator might let you accept cards, plus mobile wallets, bank transfers, BNPL, crypto (via an exchange integration), etc. For example, a platform like Corefy or Spreedly advertises integration with 100+ payment options. This breadth means you can serve customers globally with local options, all via one system.

Smart Routing & Load Balancing:

Gateway: Has no concept of routing beyond sending the transaction to the configured processor. If that processor declines or goes down, the gateway itself won’t try a different one (because it doesn’t have alternatives).

Orchestration: Dynamic routing is a core feature. The platform can route transactions to different providers based on rules or performance, and do cascading retries on failure. For instance: if Gateway A declines, automatically retry via Gateway B. A gateway alone cannot do that; the merchant would have to catch the decline and then manually call another gateway’s API (which is not practical in real-time user checkout). Orchestration automates that process, improving success rates.

Data and Analytics:

Gateway: Provides data related to transactions processed through it, usually accessible via portal or reports. But it’s siloed to that gateway. If you use two gateways, you have to compare reports yourself. Some gateways have decent analytics, but again only for their slice.

Orchestration: Because it centralizes all transactions, it can provide consolidated analytics and insights across all providers and methods. Many orchestration platforms offer advanced reporting dashboards, sometimes with customizable KPIs. You can analyze performance of each route, compare success rates, view holistic sales data. It’s a one-stop analytics shop for payments. Also, orchestration retains more data context – since it handles the entire payment journey, you might get more nuanced data (like time taken per provider, detailed decline reasons standardized across providers, etc.). This is crucial for fine-tuning strategy.

Tokenization and Vault:

Gateway: Many gateways offer tokenization to securely store cards – but the token is usually tied to that gateway. If you switch gateways, often you can’t use the same token; customers might need to re-enter cards or you go through a data migration.

Orchestration: Provides a unified vault that’s independent of the underlying processors. A token issued by the orchestration platform can be used with any of the connected providers. This means true payment data portability and a seamless saved-card experience even if back-end providers change. Plus, if you use multiple channels (online, mobile, point-of-sale), an orchestration vault can unify tokens across them – enabling omnichannel experiences like buy online/refund in store, etc. With a gateway-centric approach, you might have separate vaults for each channel/provider.

Fraud & Security Tools:

Gateway: Many gateways have some fraud checks or offer a fraud service, but it’s generally basic (AVS, CVV checks, maybe an add-on rule-based service). If you want a top-tier fraud system, you usually integrate it separately; the gateway doesn’t inherently manage multi-layer fraud across providers.

Orchestration: Not only can it incorporate the gateway’s checks, but it often integrates with dedicated fraud prevention platforms or has built-in advanced rule engines. Crucially, an orchestrator can apply fraud checks consistently across all payment methods and leverage data from all sources to make decisions. Some orchestration platforms allow multiple fraud modules to be run (like primary and secondary). Also, any 3-D Secure authentication flows can be handled once at the orchestration layer rather than individually with each gateway. This unified approach typically yields better fraud control. You’re not limited to what one gateway can do.

Customization & Control:

Gateway: You operate within the bounds of that gateway’s features. If it doesn’t do something (like schedule recurring payments in a specific way or support a certain type of installment plan), you have no choice but to find a workaround or request that feature (and wait, possibly forever). The merchant has little control except parameters on transactions.

Orchestration: Much more merchant-controlled. You set the business logic for routing, you choose which providers get used when, you can add or remove connectors as needed. In some cases, like with self-hosted solutions, you could even customize workflows. It’s your strategy encoded in the platform, rather than the provider’s one-size-fits-all approach. This means if you want, say, to route VIP customers differently (maybe always through a high-performing acquirer), you can. If you want to temporarily shift all traffic away from a provider having technical issues, you toggle it off. With a single gateway, you’d be stuck if it has issues.

Scalability & Redundancy:

Gateway: Usually one gateway can scale technically to a lot of volume, but if you need redundancy, you have to implement multiple gateways yourself. Also, a single gateway might not scale in terms of geographic reach (maybe it performs well in NA but not in APAC).

Orchestration: Built for high scalability and fault tolerance. It inherently provides redundancy by having multiple connections. If one service fails, it can automatically shift load. Many POPs are cloud-based and can scale throughput easily (they are typically stateless transaction coordinators, scaling horizontally). For a merchant, this means peace of mind during peak times – if one processor slows down due to load, orchestrator can reroute to another without losing sales.

Implementation Complexity:

Gateway: Integrating a single gateway is simpler than an orchestration platform – one API, straightforward flows. So for a very small or simple business, a single gateway integration might be quicker.

Orchestration: Initially a bit more complex integration (since the API might be richer to allow more features) but still fairly straightforward given modern platforms. The big win is if you needed multiple gateways, integrating them one by one would actually be more work than just integrating one orchestrator that covers all. So, yes, if you absolutely will always use one provider, orchestration could be overkill. But for any moderate complexity, it saves future implementation work.

Cost Model:

Gateway: Often charge per transaction or a % markup on top of processing fees. Some are just a flat monthly + small fee per transaction. If using a full PSP like Stripe, you pay their processing fees which include gateway + acquiring + other services bundled.

Orchestration: Typically charges either a SaaS fee, or per transaction fee, or a license. It’s an added cost layer in one sense, though potentially offset by savings it brings. Importantly, some orchestration solutions (like UNAK) do not charge transaction fees at all – instead you might license the software or pay a support fee and then you pay your acquirers directly. If you go the self-managed route, you have the cost of hosting and maintaining the system, but you save on per-transaction charges to a middleman. We’ll discuss UNAK more in a moment, but cost is a factor to weigh. Using a gateway vs orchestration, one might think the gateway is cheaper (since some orchestrators layer on cost per tx), but if orchestration boosts approvals and lets you cut provider fees, it can more than pay for itself.

Vendor Lock-In:

Gateway: High lock-in. If all your tokens and recurring setups are with one gateway, switching is a project. If that gateway has an outage or policy change, you’re stuck until you can swap out. Many merchants feel beholden to their primary PSP because of this (also if they offer other services like payouts, it becomes a sticky relationship).

Orchestration: Minimizes lock-in. In fact, that’s one of its purposes – to liberate merchants from being tied to one provider. Since the orchestrator is between you and providers, you can swap out an acquirer without changing your integration or impacting customers. The orchestrator ensures your tokens and data are abstracted. So you maintain leverage and flexibility.

Now, it’s worth noting a gateway is not a “bad” thing – it’s a fundamental component of processing. In fact, even with orchestration, you are still using gateways (just multiple). Orchestration platforms often partner with or include gateways. For instance, many orchestration providers will count big PSPs (which have gateways) as integrations, and might even have their own gateway functionality built-in (especially white-label ones often say “white-label payment gateway” as part of features).

So sometimes it’s not Gateway vs Orchestration as mutually exclusive – rather, if you have an orchestration platform, you might be using multiple gateways through it. But from the merchant’s perspective, the differences above hold in terms of what you have to manage and the capabilities you gain.

Which to Use When?

If you are a small business or just starting online: A single payment gateway/PSP (like Stripe, Square, etc.) might suffice. Simplicity is key at this stage; you don’t have enough volume to worry about optimization, and offering one or two payment methods covers your base. The gateway gives you the basics quickly.

As you scale or if you’re enterprise from the get-go: If you start experiencing the pain points of a single gateway (declines you can’t fix, desire for more options, high fees, limited control), that’s the time to consider orchestration. Enterprises that operate in multiple regions, or handle large volumes, almost always graduate to orchestration because the incremental revenue saved by higher auth rates and the cost savings often measure in the millions.

Technical resources consideration: If you have an in-house tech team or can handle a more robust integration, jumping to orchestration sooner can yield benefits faster. If you don’t have much tech capability, you might stay with a simple PSP longer – however, many orchestration providers cater to non-technical integration too (some have plugins or even act as a “meta-gateway” that you just send transactions to similarly as you would a normal gateway, but they do the fancy stuff behind scenes). For example, some offer a drop-in payment form, etc.

Control vs Convenience: Using just a gateway (especially an aggregator like Stripe) is very convenient – one party does everything (merchant account, gateway, risk, etc.), but you relinquish a lot of control for that convenience. Orchestration gives you back control – you can plug in best-of-breed solutions for each part (maybe you like Adyen for Europe, Stripe for US, PayPal for some set of customers, and your own preferred fraud tool). The orchestrator coordinates all that. If you’re willing to manage or oversee a bit more to reap benefits, orchestration is the way.

Now, let’s pivot to a concrete example of an orchestration solution and why it’s beneficial in comparison: UNAK.

The UNAK Advantage in Payment Orchestration

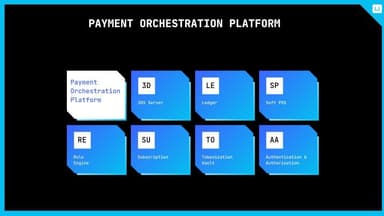

UNAK is the modular payment orchestration software developed by QaiWare, and it exemplifies many of the orchestration benefits we’ve discussed, with some standout features tailored for enterprise needs. Here’s how UNAK shines, especially vis-à-vis traditional gateway setups:

No Transaction Fees & Unlimited Volume: One of UNAK’s key strengths is that it imposes no transaction fees or volume limitations. For a merchant, this is huge. Traditional gateways and even many orchestration providers charge per transaction (or a percentage). UNAK’s model allows businesses to scale their transaction volumes without worrying about escalating costs tied to each transaction. You might pay a licensing or project fee, but you won’t have a tax on growth. In comparison, if you stick with a typical gateway that charges, say, 2.9% + 30c per transaction, you are paying more the more you sell – UNAK flips that, letting you process as much as you want for one predictable cost. In effect, this can drastically reduce your payment processing expense as a percentage of sales.

Bring Orchestration In-House: UNAK enables merchants and FIs to bring both PSP and orchestration functionality in-house. Unlike a pure SaaS gateway where you rely on the provider’s infrastructure, UNAK is built to be deployed under your control (on your cloud or data center). This means ultimate control and data ownership. You operate the platform, you set the rules – the software empowers you rather than a service constraining you. For businesses concerned about data privacy and wanting full access to payment data internally, this is ideal. All your valuable payment data sits in your databases, not scattered across provider systems. As UNAK highlights, it offers full ownership and control of valuable payment data, ensuring security and compliance while leveraging insights for growth.

Open, Agnostic Architecture with Broad Integrations: UNAK is built on an open architecture with an “unprecedented open ecosystem”. In practice, this means it’s agnostic – not tied to any single acquirer or tool – and it’s extendable. It comes with a large open catalogue of integrations and is extendable to anyone. So, whether you need to connect to a regional payment gateway, a specific bank’s API, a new fintech service, UNAK either already has it or you can integrate it. It covers payment processors, reconciliation systems, remittance, risk and fraud providers, and more in that catalogue. Traditional gateways, on the other hand, typically give you what they give you – if they don’t support a method, you can’t do much about it. With UNAK, the philosophy is you should be able to integrate “anything” payment-related into the orchestration. This future-proofs your operations and eliminates vendor lock-in comprehensively.

No Volume Constraints: Some gateways might cap you or require renegotiation after a certain volume. UNAK places no limits – you can route as many transactions as needed without hitting an artificial ceiling. For a rapidly growing business or one with seasonal spikes, that’s reassurance that your platform won’t throttle you.

Multi-Use-Case Flexibility: UNAK supports a multitude of use cases – from internal-only orchestration to building custom closed-loop payment methods. This means it’s not just for merchant payments outward. You could use it to create internal payment flows (like transferring funds between subsidiaries, or implementing an internal wallet system for your users). Closed-loop payment methods could be something like a proprietary token or credit system you want to implement – UNAK can orchestrate that alongside external methods. This breadth of use is beyond a normal gateway’s scope, showing how once you have a powerful hub like UNAK, you can innovate on payments in ways a simple gateway setup could never handle.

Economies of Scale & Cost Reduction: Because UNAK is an on-premise (or dedicated cloud) solution and eliminates per-txn fees, businesses effectively achieve economies of scale. The more you process through UNAK, the cheaper per transaction it becomes (since your costs are mostly fixed). UNAK explicitly reduces expenses in transaction processing, offering cost-effective solutions compared to traditional setups. Part of this comes from not paying markup fees, and part from being able to route to the lowest cost providers. With a single gateway, you often pay their rate for everything, which could be higher than direct bank rates. With UNAK, you can connect directly to multiple acquirers and shop for the best base rates.

Scalability and Modern Tech: UNAK touts a modern technological setup that can easily scale and adapt, while leveraging commoditized solutions. Likely, it’s built with microservices or cloud-native architecture that scales horizontally. It probably uses standard tech stacks (commoditized solutions) meaning it’s not all proprietary black box – it could be using well-understood databases, messaging, etc., which is good for reliability and for your devops to manage. Compare that to older gateway tech which might be legacy – they scale, but you don’t have insight into how, and you have to trust their scaling. With UNAK, you can design it to meet your scale needs with your own infrastructure scaling standards.

No More Transaction-Based Contracts: The combination of open architecture and no per-txn fees means you’re no longer entering revenue-sharing contracts with gateways. Instead, you have a software solution – closer to how you license an ERP or an IT platform. This can simplify procurement and forecasting. And since UNAK is PCI DSS certified, you also have a pre-certified environment for handling cards, which accelerates compliance work (you still need to maintain it, but it’s built with compliance in mind).

Real-Life Example of UNAK’s Benefits: Consider a large multi-national merchant that implemented UNAK. They were able to cut out per-transaction fees that they were paying to two different gateway providers across regions and instead paid a flat licensing fee. They connected UNAK to 8 acquirers globally (some directly, some via PSPs) and a couple of fraud services. Immediately, they saw a drop in processing cost per transaction (since no gateway markup now, and they negotiated good rates with acquirers due to volume). They also improved approval rates by routing regionally and using UNAK’s failover features – in one region, they saw an increase from 88% to 93% approval, which for their volume was enormous incremental revenue. Over a year, the ROI of switching to UNAK was extremely high – what they spent on the software and integration was recouped multiple times by savings and increased sales. Meanwhile, their teams gained richer data insights and felt more control because they weren’t filing support tickets to gateways asking “why was this transaction declined?” – they could see in UNAK’s logs exactly where it went and why it might have failed, and then adjust routing rules themselves.

In summary, UNAK combines the strengths of orchestration with a unique business model that removes transaction fees and enables full ownership. Compared to a typical gateway scenario (one provider, per-transaction cost, limited flexibility), UNAK offers:

Freedom from per-transaction costs (leading to potentially zero additional cost per transaction aside from interchange and bank fees).

Freedom to integrate any payment or fintech service (open ecosystem).

Full control to the merchant (in-house deployment, data ownership).

Scalability and reliability that meet enterprise demands.

For a merchant deciding between sticking with gateways or moving to orchestration, UNAK exemplifies why moving “up” to orchestration is beneficial: Instead of being one of many merchants constrained by a gateway’s policies and pricing, you have your own orchestration engine configured exactly to your needs and aligned with your growth.

Insights

Payment gateways vs. payment orchestration is akin to comparing a single-tool vs. an entire toolkit. A gateway can securely get a payment from point A to B (and that’s important!), but an orchestration platform can get payments from A to Z, with detours as needed, and ensure that if B fails, C is there, and so on – all while giving you oversight of the whole journey.

For modern enterprise merchants and payment professionals, orchestration isn’t just a “nice to have”; it’s increasingly the standard for competitive advantage. Gateways served us well in the early days of e-commerce, but as digital commerce has matured, the needs have outgrown what a single gateway can provide. We now operate in a world where customers demand choice, transactions cross borders daily, and uptime and optimization can make or break revenue targets. Payment orchestration is the answer to these demands, providing a unified, smart, and flexible payments infrastructure.

Platforms like UNAK push this even further – eliminating transaction fees and embracing open architecture to ensure that businesses aren’t just using an orchestration service, but truly owning their payment destiny. With UNAK, as we saw, the advantages of orchestration are maximized: no cost constraints on scaling, no vendor lock-in, and every integration you need at your fingertips in an open ecosystem.

In conclusion, if you’re weighing gateway vs orchestration:

Choose a payment gateway for simplicity when starting out or if your needs are very limited.

Choose a payment orchestration platform when you need more – more payment options, more reliability, more control, more savings at scale.

And if you want the benefits of orchestration without the usual transaction fees and with total control, solutions like UNAK provide a compelling path. They empower you to transform your payments function from a cost center into a competitive advantage – optimizing every transaction for success and cost, and positioning your business for global growth with a future-proof payment hub.

Share:

Qaiware

Payment solution expert

OVER 15+ YEARS WE ARE BUILDING COMPLEX PAYMENT PRODUCTS FOR BLUE CHIP CLIENTS